A crypto ETF lets you hold the price of a coin like Bitcoin or Ethereum inside an ordinary brokerage or retirement account, without a wallet, a seed phrase, or an exchange login. You buy a share the way you buy a stock, and a fund company holds the underlying coins (or, in older products, futures contracts) on your behalf. The convenience is real, and for a lot of people it is the whole reason to use one. So is the cost. You pay a yearly fee, you own a share of a trust rather than the coin itself, and you give up staking rewards along with any way to move, lend, or spend the asset on-chain.

That tradeoff is no longer a thought experiment. It is a menu you can order from today. US spot Bitcoin ETFs arrived in early 2024, spot Ethereum ETFs followed within the same year, and the category has since pushed past the two largest coins. Single-token wrappers for other assets, such as VanEck's spot BNB fund (ticker VBNB), have reached US exchanges. So the question is no longer whether you can buy crypto through a brokerage. It is whether you should, and which version fits what you actually want the coin to do.

This page is the version most explainers skip: plain about what these funds are, plainer about what they leave out, and built around a decision framework rather than a sales pitch or a sermon. Read it once and you should be able to explain a crypto ETF to someone else, correctly, in your own words. Below it sits our latest reporting on specific funds and filings.

- A crypto ETF gives you a coin's price exposure inside a normal brokerage or retirement account, with no wallet to manage.

- You own a share of a trust, not the coin. Only large institutions can redeem shares for the actual asset; you can only sell for cash.

- Spot ETFs hold the real coin; futures ETFs hold contracts and can quietly lose ground to the coin over time through a cost called contango.

- Most spot Ethereum ETFs do not pass on staking rewards, so you forfeit yield a direct holder would earn. Newer staking ETFs share some of it but keep a cut.

- An ETF is a way to access an asset, not a better version of it. Decide whether you want the coin first, then decide whether the wrapper is worth its fee.

What is a crypto ETF?

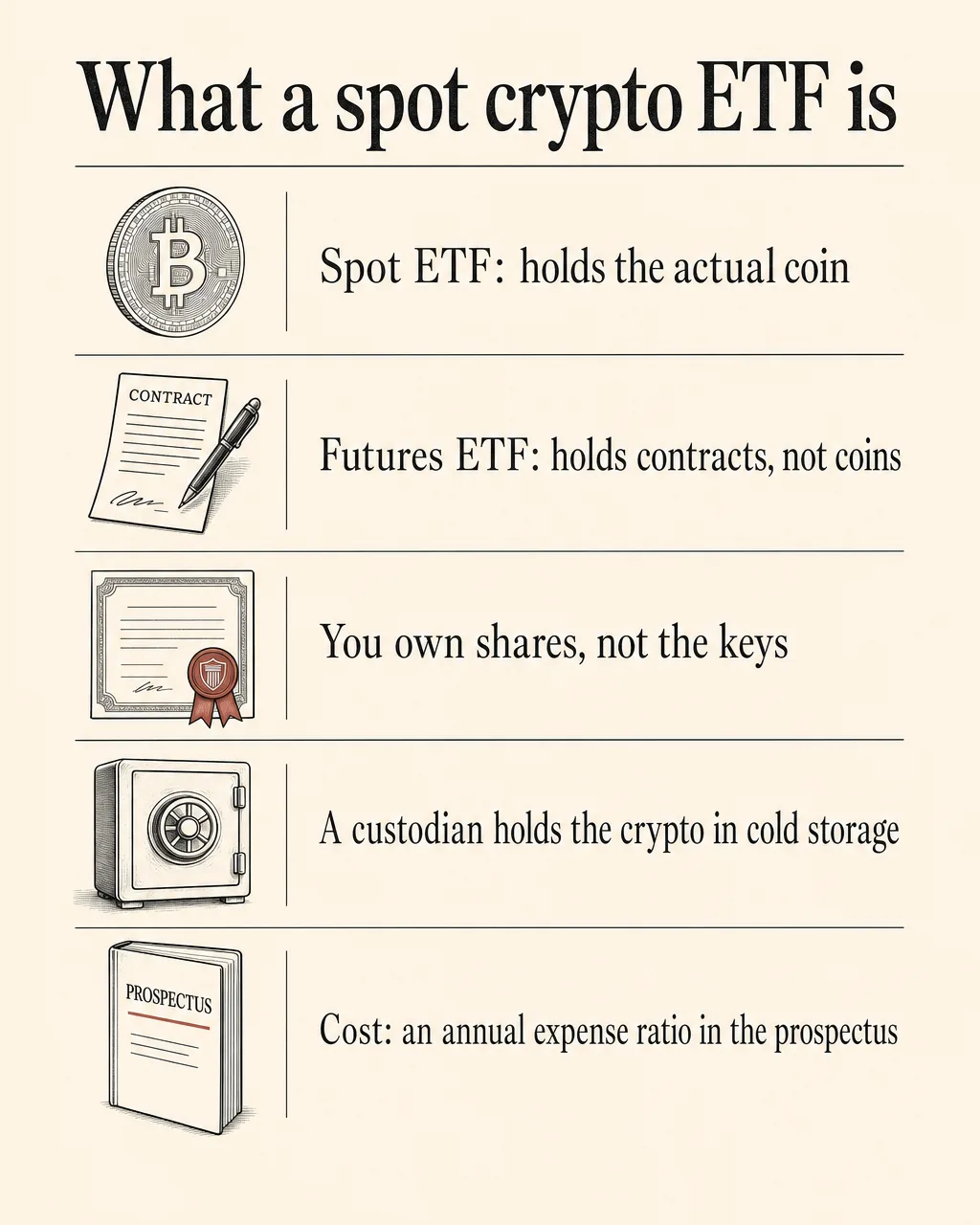

A crypto ETF is an exchange-traded fund that gives you exposure to a cryptocurrency through a share you buy and sell in a brokerage account. The fund holds the asset (or contracts tied to its price), and the share value tracks that asset, so you get the price movement of Bitcoin or another coin without ever touching the coin yourself.

Start with the two words doing the work. An exchange-traded fund is a basket of something, in this case a single cryptocurrency, that trades on a stock exchange like a share of a company. You buy and sell it during market hours through the same broker you might already use for index funds or stocks. The fund's job is to track the price of the thing it holds, so when the coin moves, the share is meant to move with it.

The appeal is access, and it is genuine. The share sits in the same account as your other investments, shows up on your normal statements and tax documents, and can often go inside a tax-advantaged retirement account such as an IRA, which is awkward or impossible with a coin you hold yourself. There is no wallet to set up, no seed phrase to safeguard, no exchange account to fund and secure. For someone who wants the price exposure and none of the operational risk, that is a real simplification.

Here is the part that gets skimmed, and it matters more than any fee. When you buy a share, you do not own Bitcoin. You own a unit of a trust, and the trust owns the Bitcoin. Think of it like a coat check. You hand over your coat, you get a ticket, and the ticket is genuinely worth a coat. But you cannot wear the ticket, and you can only get your specific coat back under the rules of the cloakroom. With a crypto ETF, the rules are strict. Only large institutions, called authorized participants, can hand shares back to the fund in exchange for the underlying coins. A retail holder cannot. You can sell your shares for cash at any time the market is open; you cannot withdraw the coin itself.

For many people this is a feature, not a bug. They never wanted to hold the coin directly. But if part of what drew you to crypto was holding an asset no company or intermediary controls, an ETF inverts that completely. You are trusting a fund and its custodian, by design.

That distinction shapes everything else on this page. The fee, the staking question, the custody question, the comparison with buying directly: each one comes back to the same fact. You hold a claim on a fund, and the fund holds the coin.

Spot vs futures ETF: the difference that matters

A spot ETF holds the actual coin. A futures ETF holds contracts that track the coin's expected future price. They sound interchangeable and they are not, and over months and years the gap between them can quietly cost you money.

A spot Bitcoin ETF buys and stores real Bitcoin. One share represents a slice of a pile of coins sitting with a custodian, so when Bitcoin's price moves, the share moves with it, minus the fund's fee. The relationship is direct. There is the coin, there is the share, and the share is a thin wrapper around the coin.

A futures ETF never touches a coin. It buys futures contracts, which are agreements to buy or sell Bitcoin at a set price on a set future date. Contracts expire. To stay invested, the fund sells contracts as they near expiry and buys later-dated ones, a routine the industry calls rolling. That is where the trouble hides. In crypto, longer-dated futures often trade at a higher price than the coin costs right now, a condition called contango. When a market is in contango, the fund keeps selling cheaper, soon-to-expire contracts and buying pricier, later-dated ones, and it loses a little value on each roll. That recurring loss is roll drag, sometimes just called contango drag.

The result is that a futures ETF can underperform the actual coin over time, even though its marketing says it tracks the same asset. The fund did nothing wrong. The structure did it. Before US spot Bitcoin ETFs arrived, a futures product was the only US ETF route to Bitcoin exposure, and some holders absorbed roll drag for a long stretch without ever knowing the word for what was happening to their returns.

For a buy-and-hold position, a spot ETF is almost always the cleaner choice, because it tracks the coin directly without the drag. Futures products can still suit short-term traders who want the exposure for days or weeks and are not holding through repeated rolls. But contango is the reason "it tracks Bitcoin" deserves a second look. Before you buy any crypto ETF, confirm in plain language whether it holds the coin or the contracts. If it is not obvious from the fund's own name and summary, treat that as a reason to keep reading the prospectus, not a detail to skip.

How do spot ETFs actually hold the coins? The custody question

Spot crypto ETFs store the underlying coins with a qualified custodian, usually in cold storage, meaning the keys that control the coins are kept offline to cut the risk of theft. This is the security backbone of the product. It also hides a concentration question that almost no beginner guide names.

First, the mechanics, because the vocabulary matters. A cryptocurrency is controlled by a private key, a secret string that authorizes moving the coins. Whoever holds the key controls the asset. Cold storage means keeping that key on hardware that is disconnected from the internet, which defends against the most common attacks, where someone drains a wallet remotely over the network. A qualified custodian is a regulated company contracted to hold the asset, keep the keys safe, and prove the coins are actually there. For a fund holding a large amount of crypto, this is the serious, unglamorous part of the operation, and the good custodians are very good at it.

Now the catch, stated plainly. Across many spot Bitcoin ETFs, the custody model looks nearly identical even when the fund issuers compete fiercely on fees and marketing. A large share of US spot Bitcoin ETF assets is held by a small number of custodians, and several funds that present themselves as rivals lean on the same company for the one thing that matters most: actually holding the coins. That has a practical consequence most people miss. Buying three different Bitcoin ETF tickers may feel like spreading your risk, but if the coins behind all three sit in the same vault, run by the same custodian, you have less real diversification of custody risk than the three tickers suggest.

Holding several different crypto ETFs does not automatically spread your custody risk. The coins behind funds that look like competitors can end up with the same custodian. If concentration matters to you, check who actually holds each fund's assets in its disclosures, not just whose logo is on the ticker.

And the point from the first section returns here. The custodian holds those coins for the fund, not for you. You hold shares. You cannot present them to the custodian and walk away with Bitcoin. That is not a flaw in any single fund; it is how the product is built. It is worth understanding before you decide that an ETF is the same thing as owning the coin, because in the way that matters most to some people, it is not.

Ethereum ETFs and the staking gap

Spot Ethereum ETFs let you hold ETH price exposure in a brokerage account, with the same trust-share structure as a Bitcoin ETF. They carry one extra cost that is easy to miss and rarely explained: most do not pass on staking rewards, so you forfeit yield that holding ETH directly would earn.

Here is the mechanism, defined before it is used. Ethereum runs on a system called proof of stake. Instead of miners competing with electricity, the network is secured by holders who lock up, or stake, their ETH to help validate transactions. In return, the network pays them rewards, in more ETH. Hold ETH yourself, or hold it through a service that stakes on your behalf, and you capture that yield. It is one of the real reasons people hold ETH rather than only trading its price.

Now hold the same ETH through most spot Ethereum ETFs, and you do not capture it. The fund holds the ETH, but it does not stake the coins and pass the rewards through to shareholders, so the yield an on-chain holder would earn is simply left on the table. You get the price exposure. You do not get the income.

This compounds with the fee in a way that is easy to overlook. You pay the annual expense ratio every year, and you give up the staking yield every year, and over a long holding period that combined gap, the fee you pay plus the yield you forgo, can grow into a meaningful difference against owning and staking the coin yourself. It is not dramatic in any single month. It adds up the way a small leak does.

A newer class of staking ETFs has started to address the missing yield by actually staking the fund's ETH and passing some of the rewards through to shareholders. That closes part of the gap. But these funds keep a portion of the rewards as a fee, so the yield is no longer fully forfeited and no longer fully yours either. The split varies by fund, and the only reliable way to know what you would actually receive is the prospectus.

What this does not mean is that an ETH ETF is a bad product. It means the staking question is a real cost that belongs in your decision. If yield is part of why you want ETH, read any Ethereum ETF's prospectus on staking before you assume the wrapper delivers it. The honest summary is simple. A plain spot ETH ETF gives you ETH's price and not its yield. A staking ETF gives you the price and a share of the yield. Direct ownership, done carefully, can give you both, and asks more of you in return.

BNB and beyond: the altcoin ETF frontier

Crypto ETFs are no longer only a Bitcoin and Ethereum story. Single-token wrappers for other coins have reached US exchanges, and VanEck's spot BNB fund, ticker VBNB, is one recent example. The headline writes itself: a coin that once lived only on crypto exchanges now trades through a brokerage account. The tradeoffs, though, do not change with the coin. They travel with the wrapper.

A spot altcoin ETF works just like a spot Bitcoin ETF. It holds the real coin with a qualified custodian, and the share tracks the price. Which means the same three caveats from the sections above apply to every single one of them, without exception. You own a trust share, not the coin. You pay a yearly fee. And if the coin runs on proof of stake, the ETF may not pass staking rewards through to you, the same gap that shows up with Ethereum.

So the arrival of a BNB ETF, or any altcoin ETF, is best read as a distribution change, not a quality signal. A coin that was previously reachable only through a crypto exchange is now reachable from a standard brokerage account. That is a real shift in access, and it is worth knowing about. But it tells you nothing about whether the coin is a sound investment. A wrapper is a delivery mechanism. It does not vet the asset inside it, it does not reduce the asset's volatility, and it does not erase the staking, custody, and control costs baked into the structure.

The clean way to think about it: each new altcoin ETF is the same machine pointed at a different coin. The machine is the trust-share-and-custodian structure you now understand. The coin is a separate question entirely. Judge the asset on its own merits, the same way you would whether or not an ETF existed for it, and let the wrapper be a convenience question, not a confidence signal. Our coverage of VBNB and the funds behind it sits below this page as the live example.

Fees: what you actually pay

Every ETF charges an annual fee, called the expense ratio, taken quietly from the fund's assets rather than billed to you directly. Across crypto ETFs, fees range from a small fraction of a percent to over a full percent a year, and that spread compounds into real money the longer you hold.

The reason the fee is easy to ignore is that you never get an invoice for it. The fund subtracts the fee from its own assets, a little each day, so your share is simply worth slightly less each year than it would be if the fund were free. On a small position held for a few weeks, the difference between a cheap fund and an expensive one is minor, the kind of thing not worth losing sleep over. On a large position held for years, it is a different story, because the fee is charged on the full value of your holding every single year, not once at purchase. Over a long horizon, the gap between a low-fee and a high-fee fund tracking the very same coin can run into real money.

There are two pieces of fine print worth your attention, because the headline fee is not always the fee you end up paying.

- A low advertised expense ratio genuinely saves money over a long hold, and on a big position the saving is not trivial.

- Larger, heavily traded funds tend to have a tighter gap between their buy and sell prices, so each trade costs you less.

- Some funds advertise a temporary fee waiver, a window where the fee is cut or zeroed before the full rate kicks in. The rate you bought on may not be the rate you pay later.

- The cheapest fund is not automatically the best deal if it is small or thinly traded. A wide bid-ask spread, the gap between the buy and sell price, can cost more per trade than you save on the fee.

The practical move is unglamorous and reliable: confirm the current expense ratio, and check whether any advertised low rate is a waiver with an expiry date, in the fund's own prospectus before you buy. The marketing page shows you the number the fund wants you to see. The prospectus shows you the number you will actually pay, and when it might change.

Crypto ETF vs buying directly: the honest comparison

Buying a crypto ETF and buying the coin directly are not the same trade with different paperwork. They carry different rights, different costs, and different risks, and the right choice depends entirely on what you want. Here is the comparison laid out plainly, point by point.

| What you are comparing | Crypto ETF | Buying the coin directly |

|---|---|---|

| Access | Lives in your brokerage account; can often go in a retirement account; no wallet needed | Needs a wallet you control and, for safety, a hardware wallet for the keys |

| Cost | Recurring annual fee for as long as you hold | One-time trading or spread cost; no ongoing fee |

| Control | You can only buy or sell the share for cash | You can move, spend, lend, stake, or use the coin on-chain |

| Yield | Most spot ETFs pass on no staking rewards; staking ETFs keep a cut | You can earn staking rewards on proof-of-stake coins |

| Custody risk | Handed to a professional custodian; safer from your own mistakes | On you; lose the keys and the coins are gone |

| Tax | Inside a retirement account, gains can be tax-deferred | Same capital-gains treatment in a taxable account |

The table is the summary. The detail underneath each row is where the real decision lives.

Access is where the ETF wins outright. It sits in the brokerage account you may already have, it can often go inside a tax-advantaged retirement account, and it asks nothing of you operationally. Buying directly means a wallet you control, and for safe self-custody, a hardware wallet like the Ledger Nano X to keep your private keys offline and out of reach of online attackers. That is more setup and more responsibility.

Cost flips the advantage. Direct ownership has a one-time trading or spread cost when you buy, and after that, no recurring fee. The ETF charges its expense ratio every year you hold, which over a long horizon can add up to far more than a single direct purchase would have cost.

Control is the sharpest split of all, and the one people underestimate. Hold the coin yourself and you can move it, spend it, lend it, use it across on-chain apps, and stake it where the network allows. Hold the ETF and you can do exactly one thing with it: buy or sell the share for cash. Everything else the coin can do is unavailable to you.

Yield, again, matters for proof-of-stake coins like Ethereum. Direct holders can earn staking rewards. Most spot ETFs pass none through, so you forfeit that yield, and even staking ETFs keep a cut. If income from the coin is part of your reason for holding it, this row may decide the question on its own.

Custody risk cuts both ways, and this is where honesty matters most. Direct ownership puts the risk squarely on you. Lose your seed phrase or send to the wrong address, and the coins are gone, with no support line to call and no reversal. The ETF hands that risk to a professional custodian, which genuinely protects you against your own mistakes. But it swaps "your keys, your coins" for "your shares, the fund's coins," and that is a real trade, not a free upgrade. If self-custody is the route you choose, our crypto safety guide covers the mistakes that actually cost people their coins.

Tax depends on your account and your country, and this is the one place to be careful with any rule of thumb. Both routes can be taxable when you sell at a gain. The standout difference is that holding an ETF inside a tax-advantaged retirement account can defer tax on gains in a way that is hard to match with directly held coins. The specifics vary enough that this is a question for a qualified tax adviser, not a web page.

Are crypto ETFs a good investment? A framework, not a verdict

There is no single answer, and anyone who gives you one is selling something. The right choice depends on what you want the coin to do and which account you want to hold it in. So instead of a verdict, here are three reader profiles. Find the one closest to you, and the tradeoff usually resolves itself.

The retirement-account holder. You want crypto price exposure inside an IRA or a similar account, and you have no interest in wallets, staking, or on-chain activity. The ETF is built for you. The annual fee and any forfeited staking yield are the price of access that direct ownership cannot easily provide inside a tax-advantaged account. For this reader, the wrapper's cost buys something direct ownership genuinely struggles to offer, and that is a fair trade.

The long-term taxable holder. You plan to buy and hold for years in an ordinary account, and you are weighing cost against convenience. This is the profile where the numbers deserve a hard look. The recurring expense ratio over your full holding period, plus any staking yield you forgo, is the true price of the wrapper compared with a one-time purchase you custody yourself. Run that comparison honestly. If the running cost is worth not having to manage a wallet, the ETF is a reasonable choice. If it is not, direct ownership with a hardware wallet keeps more of the upside in your hands.

The active on-chain user. You want to stake, lend, use on-chain apps, spend the coin, or simply hold an asset no intermediary controls. For you, the ETF cannot do any of that. It is the wrong tool, full stop, no matter how low the fee. If you are newer to holding crypto yourself, our guide to buying crypto is a sound place to start, and stablecoins are worth understanding too if you plan to move value on-chain.

One idea ties all three profiles together, and it is the single most useful thing to carry away from this page. An ETF is distribution, not alpha. It is a way to deliver an asset into your account; it is not a better or safer version of the asset. It does not improve the coin's prospects, and it does not beat the coin's own return. By design it trails the coin slightly, by the fee and any forfeited yield. So split the decision in two. First, decide whether you believe in the asset at all, on its own merits. Only then, separately, decide whether the wrapper's convenience is worth its cost. Collapsing those two questions into one is how people end up paying a yearly fee for a coin they were never sure they wanted.